Foreign investment flows to Africa slightly declined in 2023, but significant investments in the clean energy sector offered a positive highlight.

© Shutterstock/Hryshchyshen Serhii

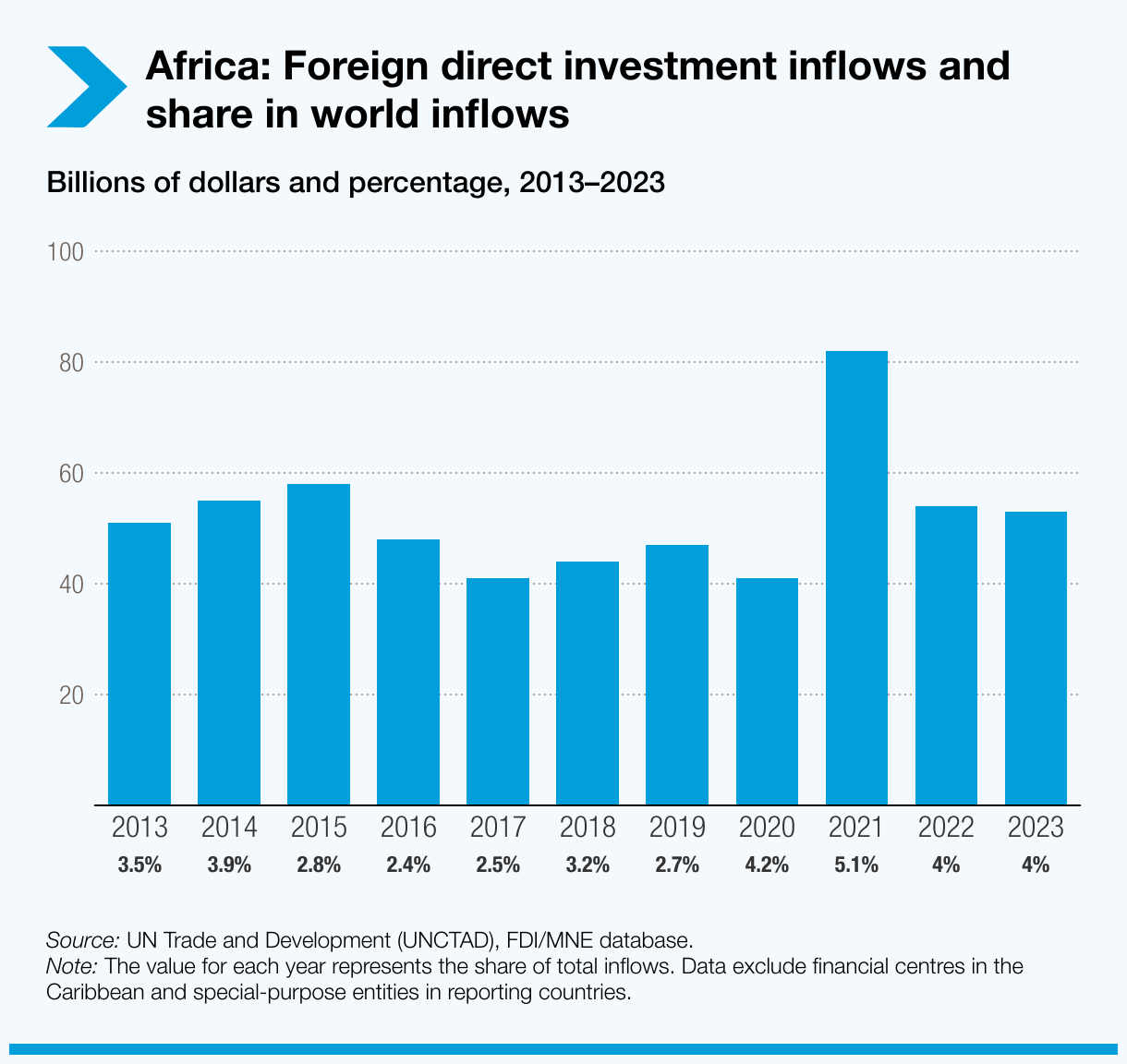

Foreign direct investment (FDI) flows to Africa fell by 3% to $53 billion in 2023, according to the latest World Investment Report released on 20 June. Two of the largest recipient economies – Egypt and South Africa – drove the overall trend.

During the year, the estimated value of international project finance deals in African nations declined by 50% to $64 billion. This follows a 20% drop in 2022.

However, the continent attracted a growing share of global greenfield megaprojects, six of them valued above $5 billion.

Topping the list was a green hydrogen project in Mauritania, a least developed country in Northwest Africa. This project is expected to generate $34 billion in investment, an amount several times greater than the nation’s GDP.

Africa also received more than $10 billion in project finance for wind and solar electricity production, with the largest projects located in Egypt, South Africa, and Zimbabwe.

Value chains for electric vehicles also prompted foreign investments. The largest deals announced included one to establish a $6.4-billion electric vehicle battery manufacturing facility in Morocco.

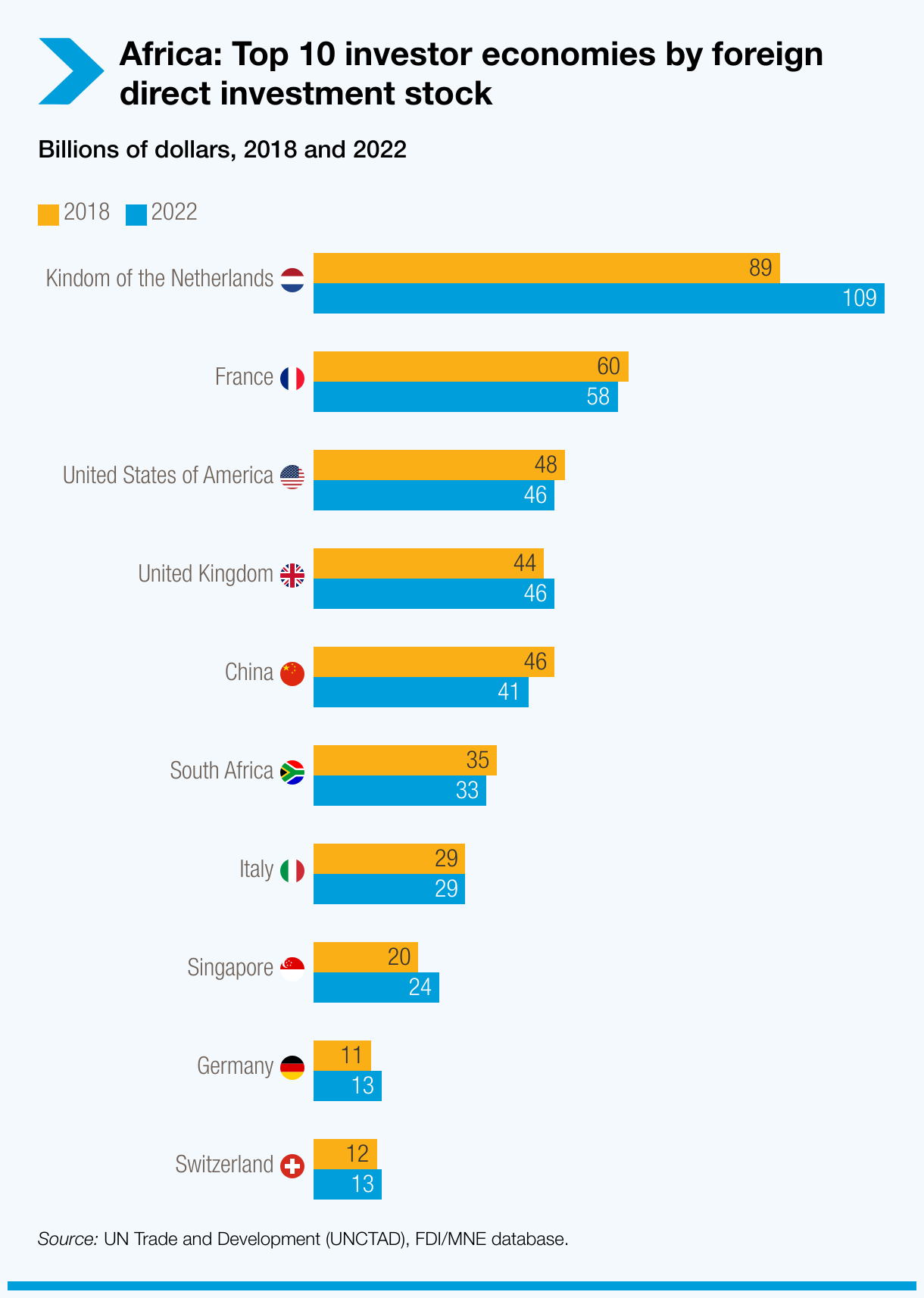

The main economies investing in the continent, by FDI stock, are the Kingdom of the Netherlands, France, the United States, the United Kingdom, and China.

How subregions fare

Foreign investments in North Africa went down by 12%. In Egypt, mergers and acquisitions fell from the highs of 2022. Morocco also had decreased FDI inflows but performed well in attracting greenfield projects.

FDI flows to West Africa dipped by 1%, with mixed results across countries. The value of greenfield investment was heavily influenced by the announced $34-billion green hydrogen project in Mauritania. Even excluding this outlier, greenfield project values tripled, and the number of projects remained stable.

In Central Africa, FDI declined by 17%. Despite a 56% increase in the number of greenfield projects and a 119% rise in their value, the region was negatively impacted by the downturn in international project finance deals.

In East Africa, FDI inflows fell by 3%, mainly due to an 11% decrease in Ethiopia. However, greenfield projects and international project finance deals increased by more than 30%, indicating better prospects ahead.

In Southern Africa, fluctuations in Angola continued to influence trends. Inflows to South Africa decreased by 43% despite higher mergers and acquisitions activity.

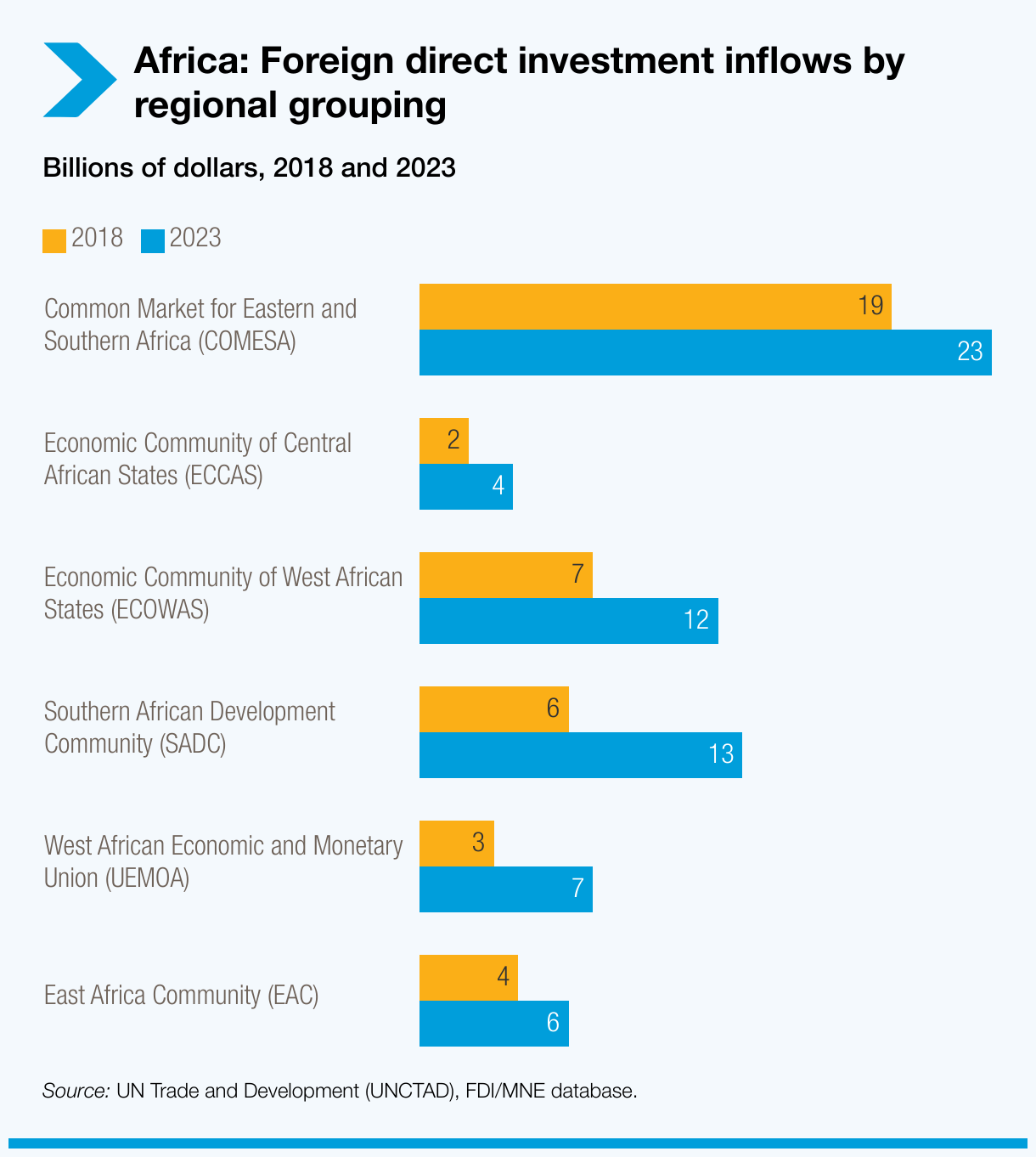

Compared to 2018, FDI inflows expanded for all major regional groupings, most prominently the Economic Community of West African States (ECOWAS), and the Southern African Development Community (SADC).