Disruptions in the Red Sea, Suez Canal, and Panama Canal have driven up shipping costs, sending shockwaves through the global economy.

Global shipping costs surged in the first half of 2024, driven by unprecedented disruptions in major maritime routes and rising operational costs.

The strain on supply chains and economies is intensifying, with vulnerable small island developing States (SIDS) and least developed countries (LDCs) facing the worst impacts.

As freight rates rise, so do concerns over trade sustainability, economic growth and the global effort to achieve sustainable development goals.

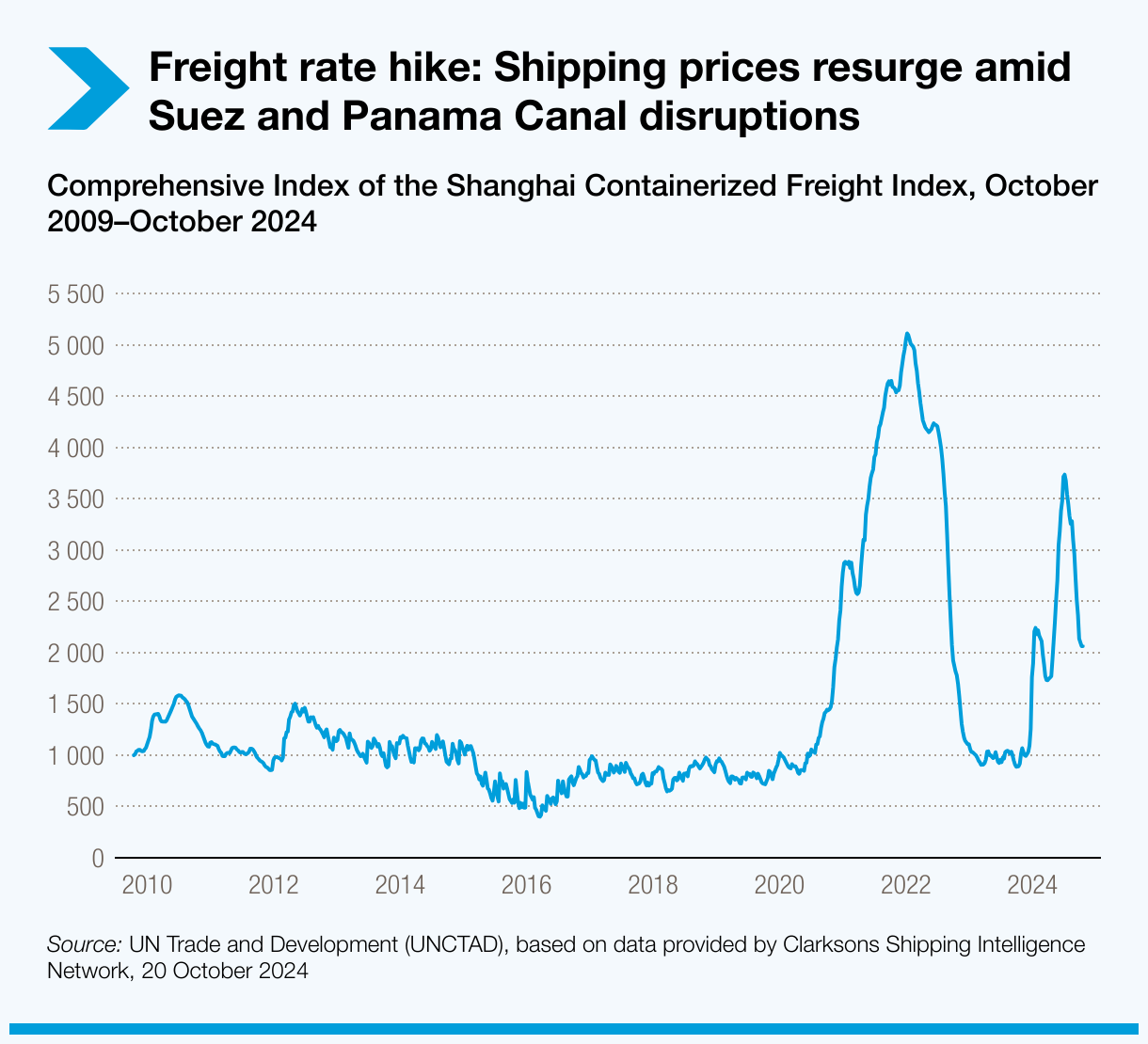

Freight rates soared amid route disruptions

Freight rates have skyrocketed in 2024 due to rerouted vessels, port congestion and higher operational costs.

By mid-2024, the Shanghai Containerized Freight Index (SCFI) had more than doubled compared to late 2023. According to the latest available data, as of 18 October 2024, the SCFI was down 45% from its 2024 high and 60% below its record level during COVID-19. However, it remained 115% above the pre-pandemic average and more than double the 2023 average.

Beyond the primary trans-Pacific and Europe-bound routes, spot freight rates also surged. From January to July 2024, the average rate on the SCFI Shanghai–South America route more than doubled to $9,026 per twenty-foot equivalent unit (TEU), the highest level since September 2022.

During the same period, the SCFI Shanghai–South Africa route saw its average rate almost triple to $5,426 per TEU (the highest since July 2022), while the SCFI Shanghai–West Africa average rate jumped 137% to $5,563 per TEU (the highest since August 2022).

Disruptions in key routes through the Red Sea, Suez Canal and Panama Canal have significantly increased freight rate volatility. Factors like increased shipping distances, heightened fuel consumption and rising insurance premiums have all contributed to a “perfect storm” of cost pressures.

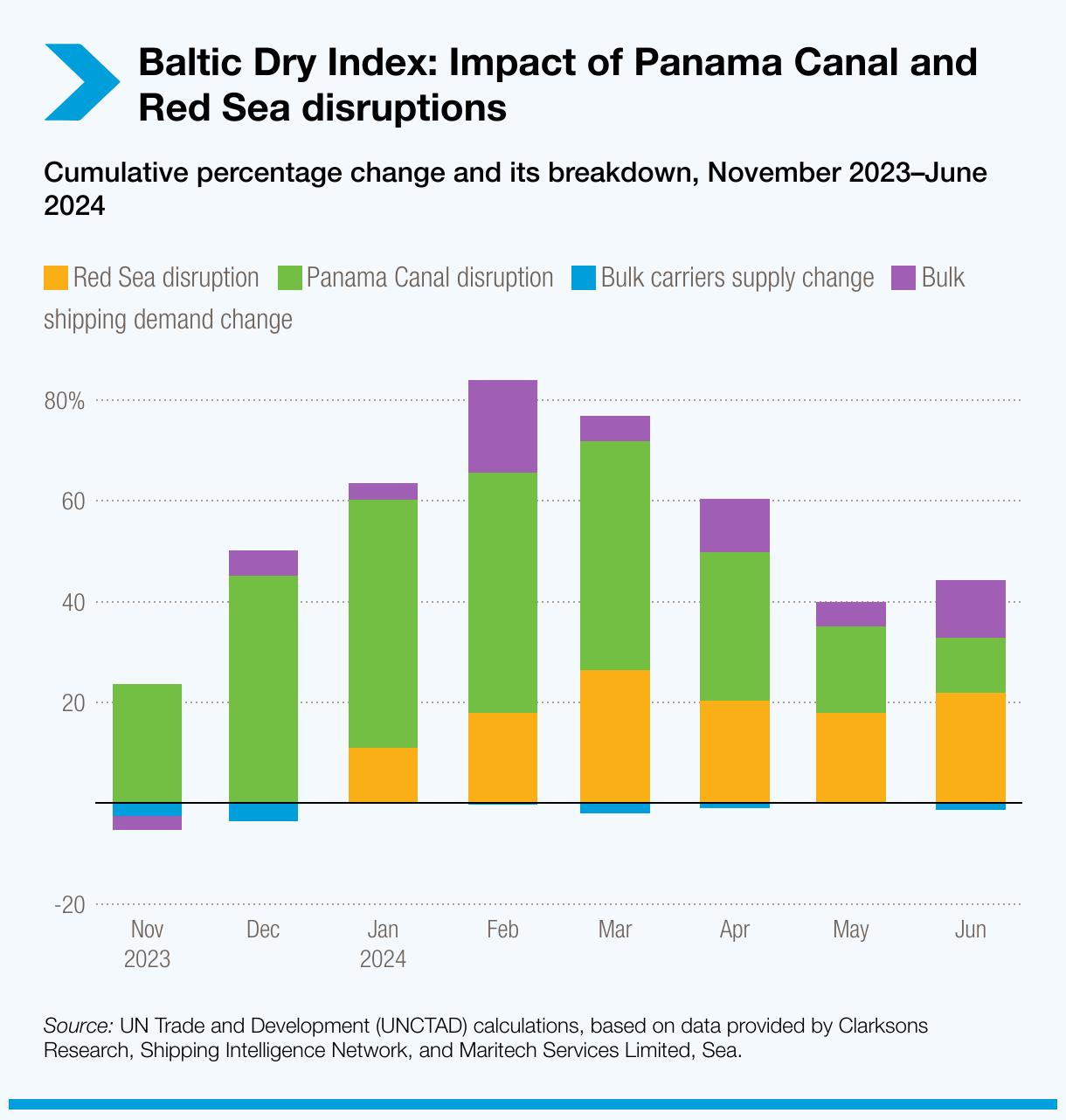

UN Trade and Development (UNCTAD) estimates show that disruptions due to climate-induced low water levels in the Panama Canal contributed 49 percentage points to the overall 45% rise in the Baltic Dry Index between October 2023 and January 2024.

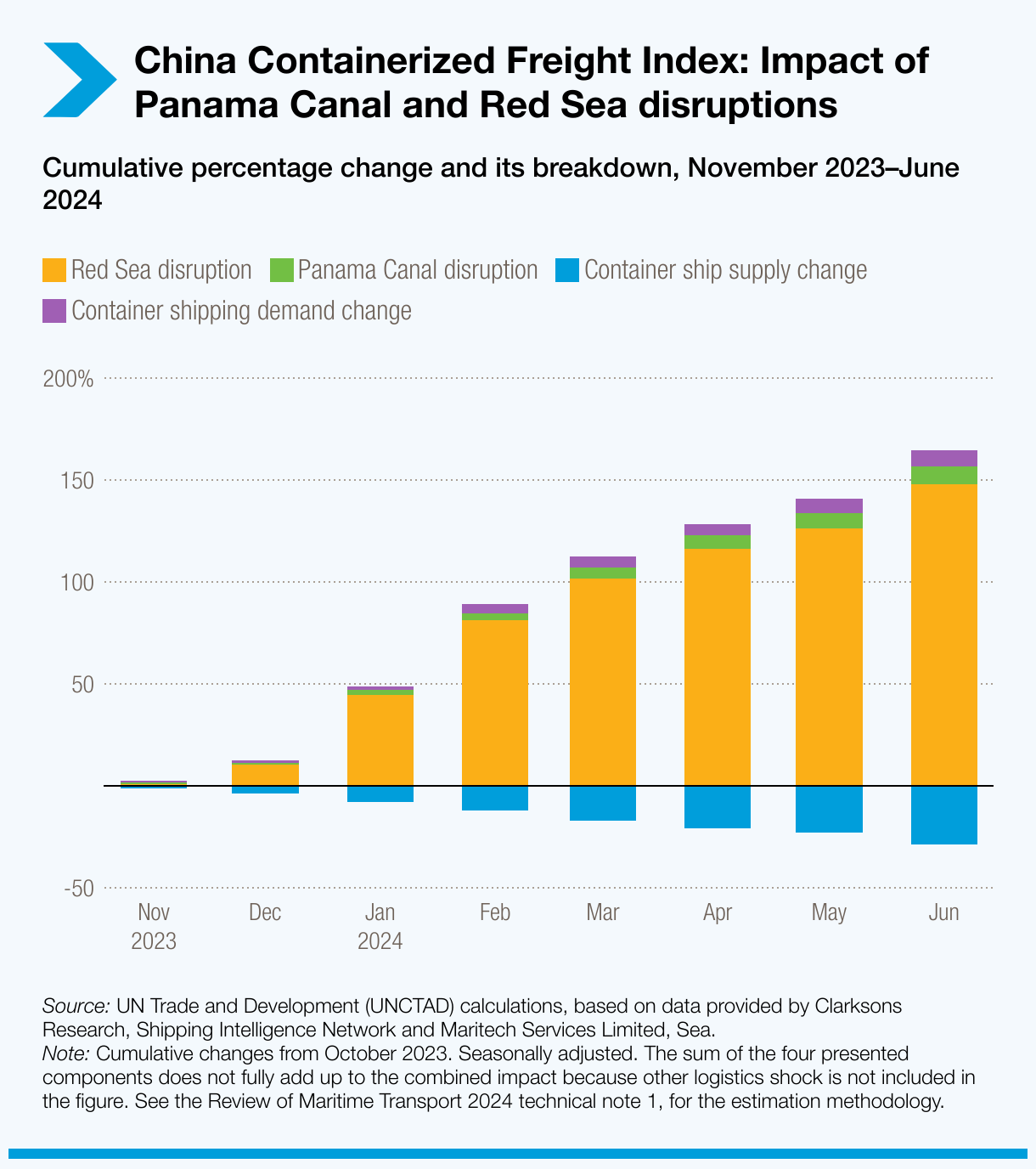

Similarly, the organization’s calculations indicate that the Red Sea crisis and Suez Canal disruptions contributed 148 percentage points to the cumulative 120% increase in the China Containerized Freight Index from October 2023 to June 2024.

Overcapacity in container shipping has mitigated rate volatility, enabling the industry to accommodate increased demand. However, any further disruptions or spikes in demand could expose risks and increase freight rates, underlining the need for effective supply management to balance supply and demand.

The impact on trade and economies

The sharp rise in freight rates is having profound ripple effects on global trade and economic stability.

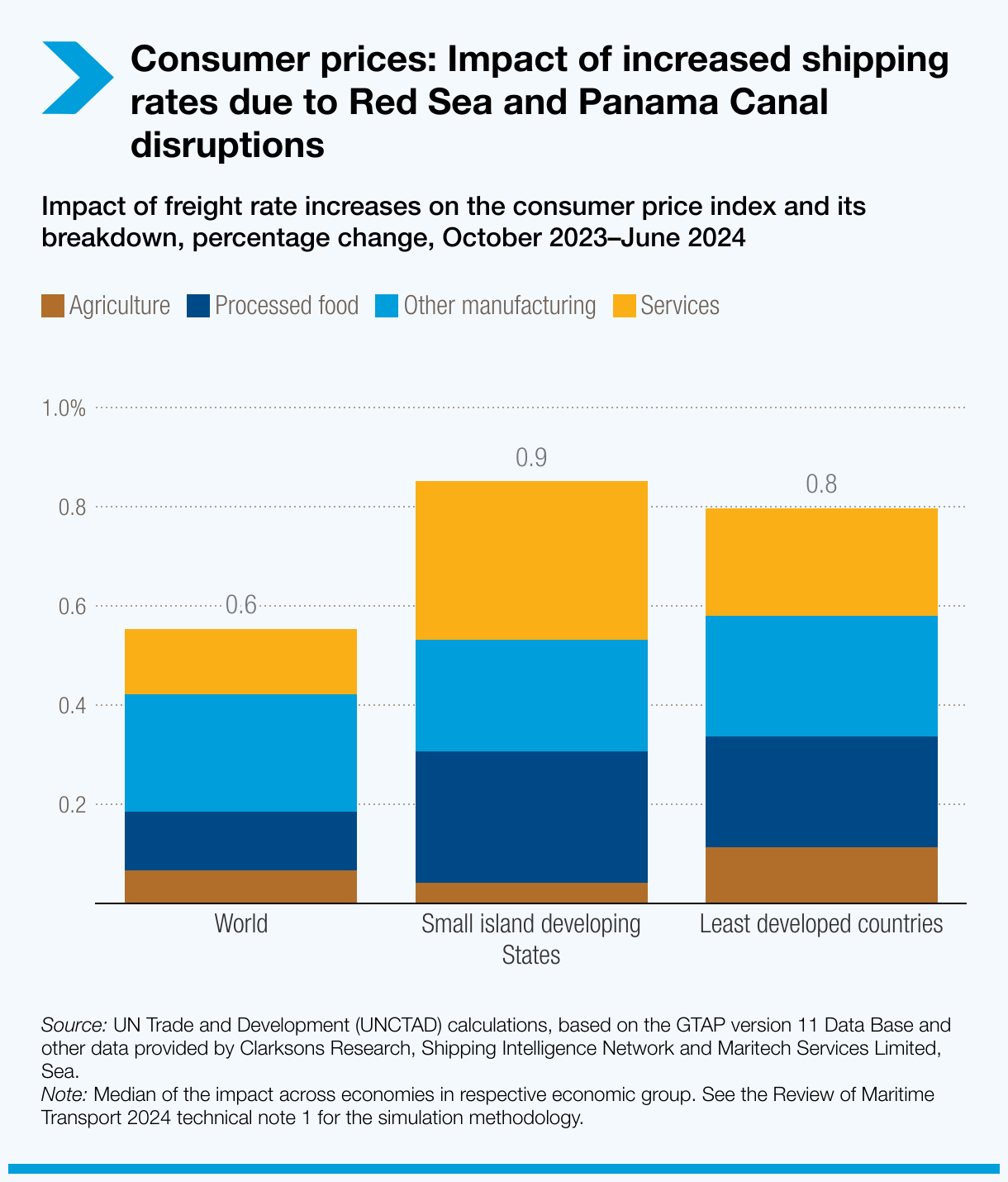

UN Trade and Development’s Review of Maritime Transport 2024 estimates that global consumer prices could increase by 0.6% by 2025 as shipping costs filter through supply chains.

Vulnerable economies like SIDS are expected to face an even sharper rise, with consumer prices climbing by up to 0.9%, threatening food security and economic growth. Processed food prices, in particular, are projected to rise by 1.3%, further exacerbating the challenges for these nations.

For SIDS and LDCs, which rely heavily on shipping for essential goods, the rising costs are eroding trade competitiveness. SIDS have already seen their maritime connectivity decline by an average of 9% over the past decade, leaving them disproportionately affected by freight rate volatility.

Urgent action needed to stabilize freight markets and support vulnerable economies

UN Trade and Development is calling for urgent, coordinated action to reduce volatility in freight markets, mitigate impacts and support vulnerable economies. This includes:

- Monitoring freight market trends to detect cost spikes early and provide timely support to vulnerable economies.

- Strengthening international cooperation to reduce chokepoint disruptions and rerouting pressures, helping to stabilize shipping routes and reduce costs.

- Investing in port and infrastructure upgrades to alleviate congestion and improve supply chain efficiency, especially in key transshipment hubs.

- Diversifying shipping routes and promoting regional trade initiatives to reduce dependence on long-distance routes, easing pressure on global shipping lanes.

- Supporting low-carbon shipping and port solutions to mitigate the environmental impacts, improve efficiency and drive a sustainable transition for the maritime industry.

Signal of deeper structural vulnerabilities

Rising freight rates represent more than just a temporary cost hike – they signal deeper structural vulnerabilities in global supply chains, such as susceptivity to heightening geopolitical tensions and climate change risks.

Without urgent action to reduce freight market volatility and address the root causes of disruptions, the economic and social impacts on vulnerable economies could be long-lasting.

By investing in resilient infrastructure, diversifying trade routes and supporting sustainable shipping and port solutions, the maritime sector can pave the way for more efficient, equitable and resilient trade.