By Paul Akiwumi, Director for Africa and Least Developed Countries, UNCTAD

©Vitoria Holdings LLC

The COVID-19 pandemic crisis has worsened the vulnerabilities caused by the excessive reliance of African economies on world markets.

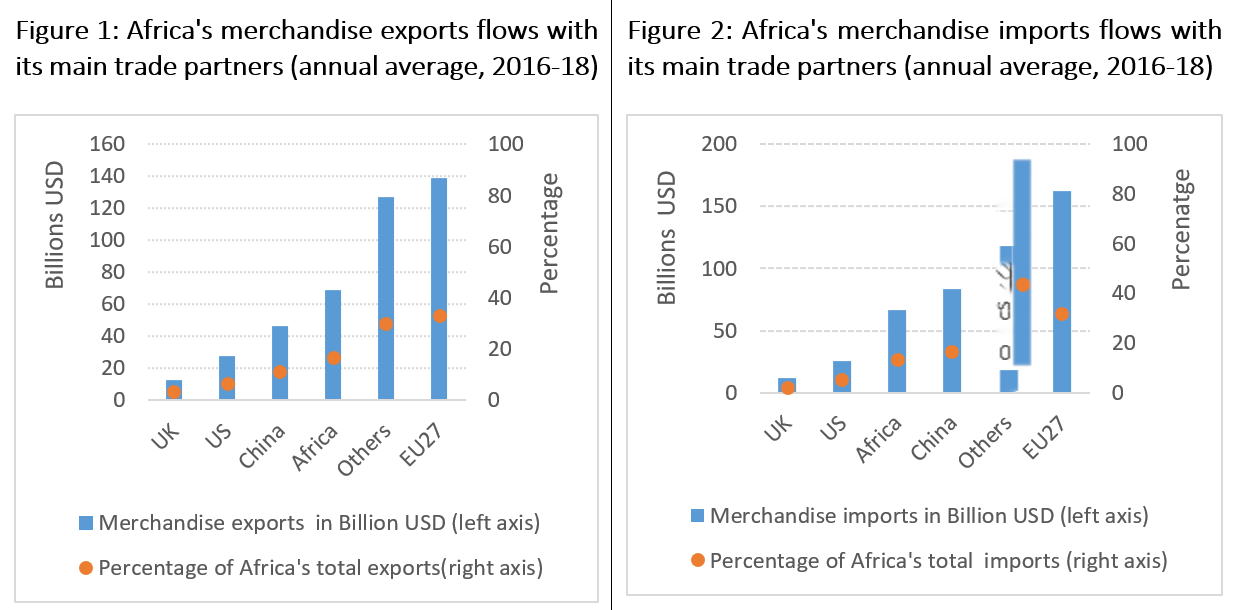

Africa’s main trade partners include the European Union, China, United States and the United Kingdom. Together they represent more than 50% of the continent’s trade flows (see figures 1 and 2 below).

Africa’s dependence on external markets for medicinal and pharmaceutical products is particularly acute – Africa imports more than 95% of these products from outside the continent.

As the continent’s main trade partners have been severely hit by the COVID-19 pandemic, Africa has suffered significant business disruptions and output contraction, including in export sectors.

Africa’s GDP could contract by 1.4% in 2020 while the continent’s total merchandise exports could decline by 17%. McKinsey estimates that Africa’s manufacturing sector output will shrink by 10% in 2020 – equivalent to a loss of more than $50 billion – as result of COVID-19.

Deeper integration can build resilient economies

Deepening regional integration on the continent through the African Continental Free Trade Area (AfCFTA) can build resilient economies post-COVID-19.

The AfCFTA, if quickly and effectively implemented, can address challenges emanating from Africa’s reliance on world markets while creating more value in local economies. This will in turn help reduce vulnerability to future pandemics.

The AfCFTA could by 2035 boost Africa’s total exports by 29%, intra-continental trade by more than 81%, and African exports to the rest of the world by 19%, with most of the gains accrued to the manufacturing sector.

However, AfCFTA implementation requires significant financial resources due to the need to address infrastructure bottlenecks, invest in productive capacities and expand access to operational cash flows by businesses.

The continent’s infrastructure financing gap ranges from $68 to $108 billion while its trade finance gap is estimated at $91 billion per annum.

Other priority actions include setting up and operationalizing institutional frameworks to coordinate the implementation and monitoring of the agreement, as well as sensitizing and developing the capacity of a wide range of actors to realize its objectives.

Africa therefore needs to mobilize more domestic capital, an effort that is often frustrated by illicit financial outflows, among other impediments.

Curbing illicit flows key to better recovery

Illicit financial flows (IFFs) drain billions of dollars out of Africa every year. Curbing these flows will contribute to increasing some of the much-needed resources required to realize the AfCFTA. In turn, the latter can provide a framework for cooperation and institutional capacity to combat IFFs.

In 2015, IFFs from the continent were estimated at $50 billion per year. UNCTAD in 2020, reckons that Africa loses about $88.6 billion per annum in illicit capital flight.

IFFs appear most prominent in the extractive sector, estimated at over $40 billion in 2015 and a cumulative amount of $278 billion from 2008 to 2018. In addition, Africa’s financial challenges are currently exacerbated by the impact of COVID-19 and scale of recovery responses.

The AfCFTA process including preparatory interventions and actual implementation (likely to begin in early 2021) coincides with the global spread of COVID-19 and its recovery.

These create a dilemma with competing priorities between AfCFTA and COVID-19 recovery requirements for budget allocation, including from additional resources recovered from IFFs. Nonetheless, building stronger post-COVID-19 African economies is linked with potential AfCFTA outcomes.

For example, curbing IFFs could possibly increase the capital available for businesses, boosting their capacities to produce and trade towards AfCFTA markets, especially at a time when the pandemic has severely hit their cashflow.

Reducing IFFs may also provide governments with the necessary additional fiscal space to provisionally support a private sector recovery from the impact of COVID-19 and fund institutional capacity arrangements and other actions needed to ensure the operationalization of the AfCFTA.

Policy collaboration required for success

Therefore, policy sequencing and synergies should be sought by countries when they are devising and implementing both AfCFTA and COVID-19 recovery strategies.

Considering the development challenges posed by IFFs and their linkages to trade and other cross-border activities, cooperation among African customs authorities, financial institutions and regulatory bodies provided under the AfCFTA offers an opportunity to track and combat these flows.

The AfCFTA could establish the foundations for better integrated actions including: the harmonization of investment laws and practices; improvement of data collection and information sharing to better track IFFs; building-up of institutional capacity; and the promotion of transparency and accountability at both the state and private sector levels which is essential to combating many forms of IFFs.

The UNCTAD Economic Development in Africa Report 2020 addresses some of these issues and provides the concrete steps that African countries should take towards building greater cooperation, including under the AfCFTA, to curb IFFs.

Read the original article on Mail and Guardian

Follow them: @mailandguardian on Twitter | @MailGuardian on Facebook