- The pandemic has seen governments in the North abandon parts of the 40-year long neo-liberal policy dogma to protect lives and livelihoods amidst the Covid-19 pandemic and an unprecedented economic contraction.

- But without a more thorough revision of multilateral rules and norms, inequality will persist, the world will squander financial resources and fail to meet the challenge of the climate crisis, even as growth returns.

- The world needs more effective multilateral coordination, without which recovery efforts in advanced countries will damage development prospects in the South and amplify existing inequalities.

- Through 2025 developing countries will be $12 trillion poorer because of the pandemic; the failure to roll out vaccines could knock another $1.5 trillion from incomes across the South.

Shifting decisively away from four decades driven by a misplaced faith in unregulated markets, and breathing new life into multilateral cooperation, will demand additional policy transformations that go well beyond the rescue packages prompted by the Covid-19 pandemic, according to the latest UNCTAD Trade and Development Report.

To their credit, governments in advanced countries have responded to the Covid-19 shock by rediscovering the power of their purse and making resilience, rather than flexibility, the metric of recovery. But the crisis has also revealed just how fragmented and fragile the global economy has become, and how far this policy shift must extend if the oft-repeated phrase “built back better” is to define the post-pandemic recovery.

Deprived of the policy independence and vaccines that advanced economies take for granted, many developing countries are facing a cycle of deflation and despair, with a lost decade looming. Through 2025 developing countries will be $12 trillion poorer because of the pandemic, according to UNCTAD; on some counts the failure to roll out vaccines will, alone, knock $1.5 trillion from incomes across the South.

“The global recovery from the pandemic must reach beyond emergency spending and infrastructure investments to embrace a reinvigorated multilateral model for trade and development,” said Rebeca Grynspan, the secretary-general of UNCTAD. “Only a concerted rethinking of priorities holds out hope of addressing the inequality and climate crises that have come to define our era.”

An examination of policy actions in three key areas of resilience building – reducing inequality, countering corporate power and reducing carbon emissions – suggests that advanced economies have taken welcome steps, but without the heft that more decisive steps and coordinated support would bring.

Back in January 1981, the recently elected US president, Ronald Reagan, promised his fellow citizens “a new beginning”. Free from government meddling and its economic afflictions, a vigorous, fairer and more productive economy would emerge. His message that “government is not the solution to our problem; government is the problem” went global.

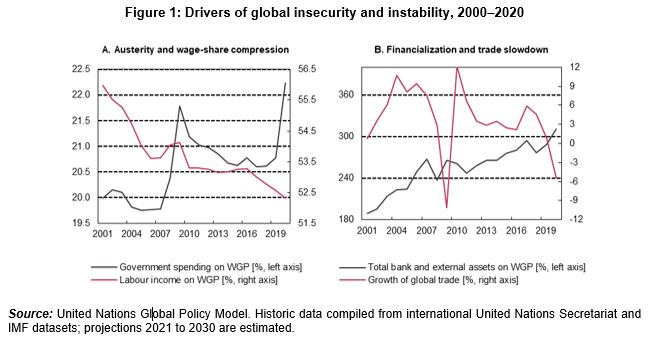

UNCTAD’s Trade and Development Report was launched that same year and has been tracking the impact of neo-liberal policies ever since. Much has changed, but at a fundamental level the warnings in the first Report – of an uncoordinated global economy prone to shocks and crises – have withstood the test of time; with creditors favoured over debtors; large producers dominating the small; profits amassed at the expense of wages; and the interests of developed countries prioritised over those of developing countries (Figure 1).

“Over the past 40 years, we’ve witnessed the emergence of a full-blown rentier economy with global reach and an addiction to debt, both public and private,” said Richard Kozul-Wright, director of UNCTAD’s globalization and development strategies division. “Not only that, inequality has become a feature of our globalized world, while concentrated private economic power erodes public authority to respond.”

Crises are, no doubt, an opportunity for change, and the last four decades have seen plenty, culminating in the 2008-09 global financial crisis. But despite the damage to employment, incomes and savings, governments failed to escape the influence of unregulated financial markets, corporate power and extremely wealthy individuals. If the post-pandemic period sees a repeat of this failure, through a combination of fiscal tightening, watered-down labour market rules, and unequal trade and investment agreements – even as monetary policy remains loose - hopes of generating a sustained, equitable boom will surely recede rapidly.

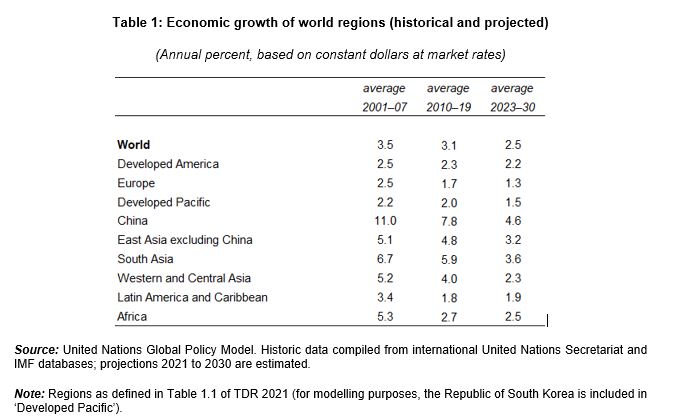

Instead, and even without another financial crash, the global economy will remain subdued for the remainder of the decade with developing countries, particularly in Africa and South Asia, hit hardest (Table 1).

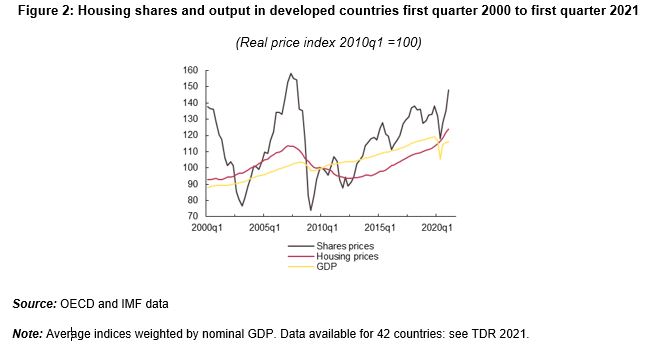

Since the global financial crisis, $25 trillion has been pumped into advanced economies, making them de facto wards of their Central Banks. The result, prior to the pandemic, was a perverse mix of slower growth and booming financial markets (Figure 2). Though governments added big fiscal packages to their policy arsenal as the pandemic struck, booming financial markets will threaten the recovery if their inflation phobia outweighs pressure to support real economic activity.

As advanced economies spring back to life after extended lockdowns, the crisis may quickly lose its global designation, but that growth will only expose the lack of cohesion of the multilateral system. The Report welcomes the agreement on a $650bn SDR allocation, which will offer some relief, but this will not be enough to reverse the downward spiral in most developing countries where, austerity remains the default policy for governments under financial pressure from footloose capital and unforgiving markets.

And on the health front, the COVAX and C-TAP schemes have been unable to mobilise the requisite resources from Northern governments and corporations, many of which have, at the same time, resisted developing country calls to temporarily waive TRIPS rules in the WTO in support of local vaccine production.

UNCTAD, as it did 40 years ago, sees greater policy coordination as a prerequisite for building back better from a serious global shock. But it also sees an urgent need to build in bolder actions, together, before it is too late. The Report draws several lessons from the crisis that could help strengthen the ambition of policy makers at the national and international levels:

- Governments are not budget constrained in the way households are, but not all governments are created equal. Developing countries need support to expand their fiscal space.

- Central Banks are public institutions authorized by the state to create credit. How they use that authority should reflect public policy decisions aimed at equitable growth.

- Resilience, therefore, is a public good. It can only be delivered through public investment.

- Finance is too important to be left to markets: public banks and stronger regulatory oversight can deliver a healthier investment climate.

- Cutting wages is bad for business and worse for society; wages are a critical source of demand, their growth can stimulate productivity and underpin a strong social contract.

- A healthy economy is a diversified economy. Industrial policy matters for countries at all levels of development. The question is not if, but how.

- A caring society is a more stable society and good social policy must go beyond offering a residual category of safety nets designed to stop those left behind from falling further.